Due to the impact of the coronavirus on semiconductor supply and demand, worldwide semiconductor revenue is forecast to decline 0.9% in 2020, according to Gartner, Inc. This is down from the previous quarter’s forecast of 12.5% growth.

“The wide spread of COVID-19 across the world and the resulting strong actions by governments to contain the spread will have a far more severe impact on demand than initially predicted,” said Richard Gordon, research practice vice president at Gartner. “This year’s forecast could have been worse, but growth in memory could prevent a steep decline.”

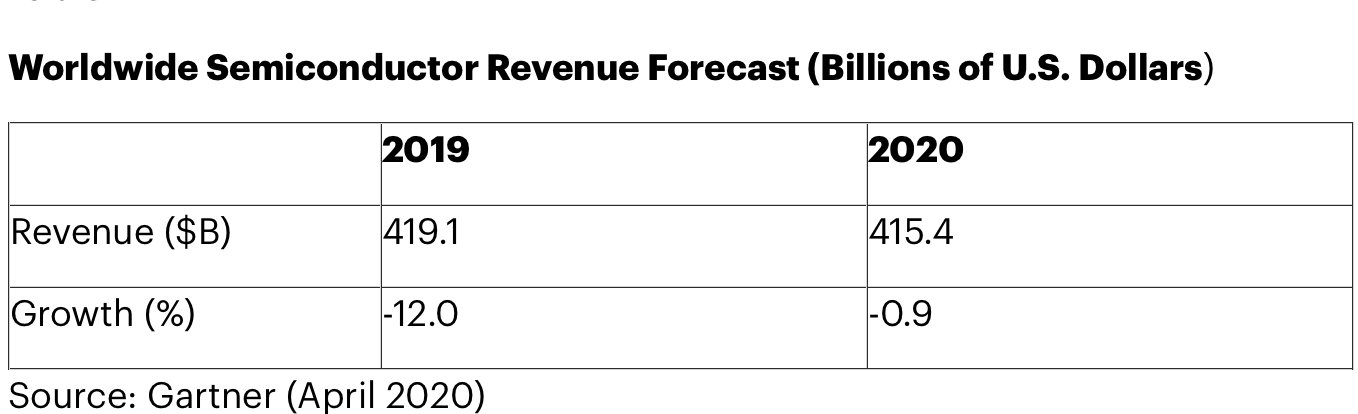

Overall, 2020 global semiconductor revenue has been reduced from the previous quarter’s forecast by $55 billion, to $415.4 billion (see Table 1). 2020 total market growth has been reduced from 12.5% to a decline of 0.9%, with non-memory expected to decline 6.1%, while memory is forecast to grow 13.9%.

Semiconductor memory revenue will account for 30% of the total worldwide semiconductor market in 2020. The memory market is forecast to reach $124.7 billion in 2020, an increase of 13.9%, while the non-memory revenue market is on pace to total $290.6 billion, a decline of 6.1% year over year.

Within memory, NAND flash revenue is forecast to grow 40% in 2020 due to severe shortages persisting from 2019, which keeps pricing firm. “NAND flash supply will remain historically low in 2020 due to fab delays and technology transitions, but the demand will diminish later in 2020,” said Gordon. “Initial price increases of 15.7% during the first half of 2020 will reverse to a 9.4% decline during the second half of the year. However, average pricing levels will still enable NAND flash revenue to achieve growth this year.”

Strong demand from cloud service providers in the first half of 2020 will push pricing and revenue higher in server DRAM. However, this growth will be more than offset by weak demand and falling prices from the smartphone market. For the DRAM market overall, Gartner analysts estimate DRAM revenue will decline 2.4% in 2020.

“Non-memory semiconductor markets will experience a significant reduction in smartphone, automobile and consumer electronics production and be heavily impacted across the board,” said Gordon. “In contrast, the hyperscale data center and communications infrastructure sectors will prove more resilient with continued strategic investment required to support increased remote working and online access.”